For many small and mid-sized businesses, traditional debt financing through banks isn’t always practical. Strict underwriting requirements, collateral demands, and lengthy approval processes often leave business owners searching for alternative options. This is where revenue-based financing solutions, such as bridge loans and merchant cash advances (MCAs), come in.

Both products provide a flexible funding solution tied to a company’s actual business revenues. Each serves a unique purpose, and understanding the differences helps business owners decide which path best fits their situation.

What Is Revenue-Based Financing?

Revenue-based financing is a form of alternative funding where repayment is directly tied to monthly revenue or daily/weekly sales. Instead of traditional fixed payments like in a bank loan, the repayment adjusts with sales performance. This makes it attractive for businesses with fluctuating income streams.

Unlike equity financing, where an investor receives partial ownership in exchange for capital, revenue-based financing allows entrepreneurs to raise funds without giving up control of their business. It combines the flexibility of variable repayment with the independence of retaining full ownership.

Bridge loans and MCAs are two of the most widely used revenue-based financing options, each offering unique advantages.

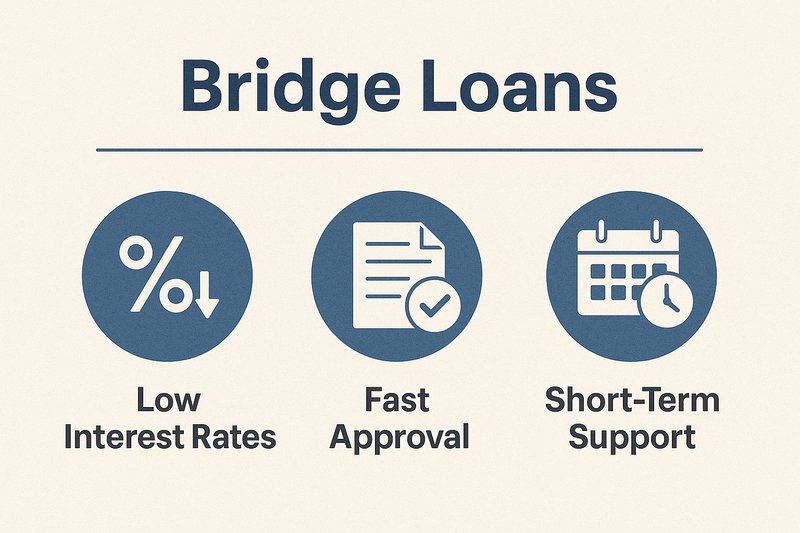

Bridge Loans: Lower-Cost, Short-Term Support

A bridge loan is often used to cover a temporary gap in cash flow until longer-term financing or receivables arrive. For many companies, it is a cost-effective way to stabilize finances without resorting to higher-priced funding.

Key Features of Bridge Loans

For Established Businesses

Most bridge loan programs are available to business owners with a credit score of 690 or higher and steady monthly revenue. This ensures the borrower has a proven track record of managing finances responsibly.

Lower Interest Rates Compared to MCAs

Because the borrower profile is stronger, bridge loans usually come with lower rates and monthly payments than MCAs. While they may not match traditional bank loan rates, they provide affordable access to short-term capital.

Fast Access

Funding can be approved within days, making bridge loans useful for businesses that need capital quickly but still qualify for competitive pricing.

Short-Term Repayment

Terms typically range from a few months up to one year. Repayment can be structured as fixed payments or tied to business revenues, depending on the program.

When to Use a Bridge Loan

Covering payroll or operational expenses while waiting on accounts receivable.

Taking advantage of supplier discounts by purchasing inventory in bulk.

Handling short-term cash flow needs until an SBA or bank loan closes.

Funding growth opportunities where revenue returns will be realized quickly.

For businesses with strong credit and consistent monthly revenue, a bridge loan offers a flexible funding solution that balances speed and affordability.

Merchant Cash Advances (MCAs): Revenue-Based Working Capital

A merchant cash advance (MCA) provides businesses with a lump sum upfront in exchange for a percentage of future revenues. Instead of fixed monthly payments, repayment is deducted automatically as a portion of daily or weekly sales.

What Makes MCAs Different?

Accessibility

MCAs are available to businesses with weaker credit profiles or limited collateral. Even if a company has been turned down for traditional debt financing, it may still qualify for an MCA if they have consistent sales.

Speed

Funding can be approved in as little as 24–72 hours, making MCAs one of the fastest forms of business financing.

Revenue-Based Repayment

Since repayment is tied directly to business revenues, payments automatically adjust with cash flow. When sales are strong, the advance is repaid more quickly; when sales dip, deductions are smaller.

No Collateral Required

Unlike secured loans, MCAs are based on sales performance rather than physical assets. This makes them accessible to service-based and online businesses.

Best Uses for MCAs

Emergency expenses such as equipment replacement.

Purchasing inventory for peak seasons.

Funding marketing campaigns that can drive immediate sales.

Bridging short-term cash flow gaps when monthly revenue is temporarily lower.

Why MCA Rates Are Higher

Because MCAs are designed for businesses with limited options, the cost of capital is typically higher than a bridge loan. Funders take on more risk by advancing money without relying on personal credit scores or collateral.

Instead of interest rates, MCAs use a factor rate. For example, a $20,000 MCA with a 1.3 factor rate requires repayment of $26,000, regardless of how quickly it’s paid back.

While this structure often leads to higher total costs, it also creates a flexible funding solution for businesses that cannot qualify for other financing.

Common Pitfalls of MCAs — and How to Avoid Them

MCAs are powerful tools, but misuse can create challenges. Here are some common pitfalls and strategies to prevent them:

Over-Borrowing

Taking out multiple MCAs can quickly overwhelm monthly revenue. Business owners should use one MCA strategically rather than stacking advances.

Funding Long-Term Projects with Short-Term Financing

MCAs are designed for short-term needs, not for projects that take years to generate returns. Using them for long-term investments can cause repayment struggles.

Ignoring Cash Flow Planning

Because payments are deducted from revenues, it’s important to ensure average daily or monthly sales can support repayment.

Not Considering Alternatives

Business owners who qualify for bridge loans or other debt financing may save significantly on costs by exploring all options first.

When used responsibly, MCAs provide a flexible funding solution that aligns with business revenues.

Real Estate Loans as Consolidation Tools

For business owners who already have multiple MCAs, repayment obligations can become overwhelming. One strategy to regain control is to use a real estate loan to consolidate MCA debt.

If the business owner has equity in property, they may qualify for a loan that consolidates several advances into a single obligation. This approach provides:

Lower rates and monthly payments compared to multiple MCAs.

A single, predictable repayment schedule with fixed payments.

The ability to stabilize cash flow and redirect revenue back into growth.

This option isn’t right for every business, but for those with real estate assets, it can be a practical way to restructure debt while maintaining access to working capital.

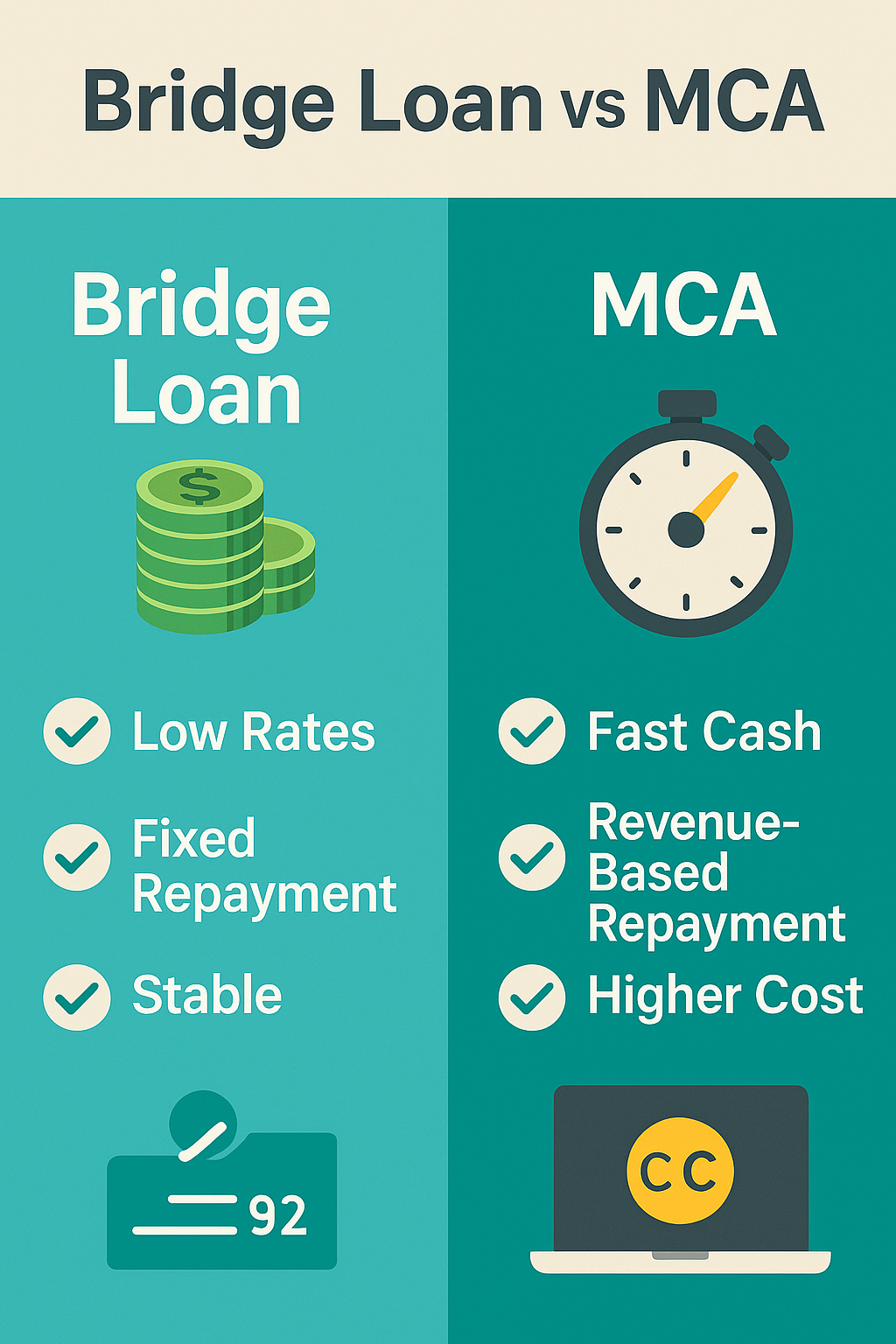

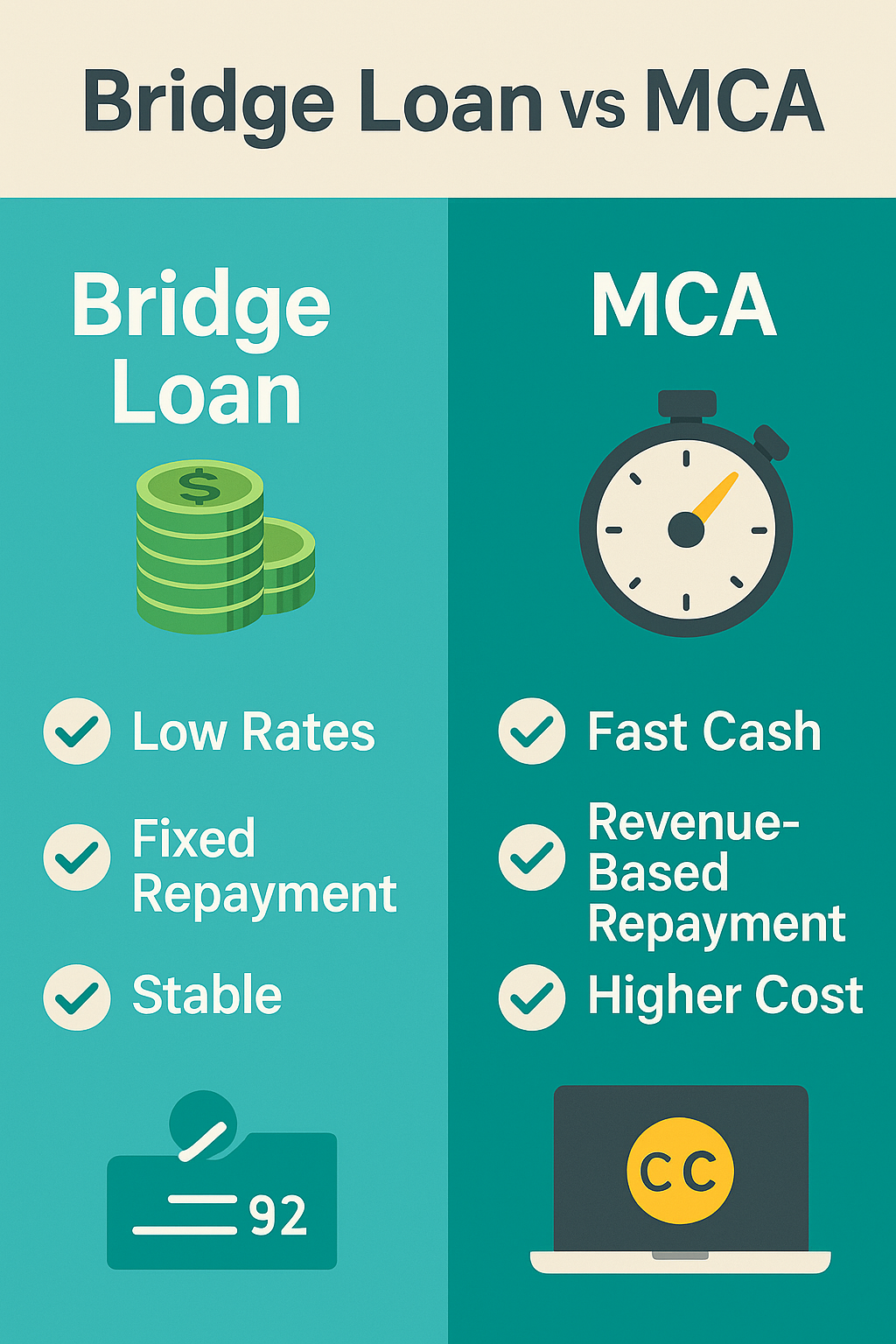

Comparing Bridge Loans and MCAs

Both bridge loans and MCAs are forms of revenue-based financing, but they cater to different circumstances.

Bridge Loans

Best for established businesses with a credit score of 690+

Lower rates and flexible repayment, monthly payments

Ideal when monthly revenue is stable and predictable

Often structured with fixed payments

Merchant Cash Advances

Available to businesses with lower credit scores

Repayment tied to business revenues

Higher overall costs but extremely fast funding

Flexible when sales fluctuate

By understanding the purpose and strengths of each, business owners can align financing with their needs rather than forcing their business model into the wrong funding option.

Conclusion

Revenue-based financing fills a vital gap for small and mid-sized businesses. Both bridge loans and MCAs are designed to meet different needs, but neither should be viewed negatively.

Bridge loans reward stronger credit and established revenues with lower interest rates and fixed monthly payments.

MCAs provide fast, accessible funding tied directly to business revenues, making them a practical choice for entrepreneurs who cannot access traditional debt financing.

Real estate loans can also serve as consolidation tools, helping businesses restructure MCA debt into manageable repayment plans.

At their core, these options are flexible funding solutions designed to help businesses grow, stabilize, and thrive. By understanding the differences and using them strategically, business owners can make smart choices that support long-term success without sacrificing control through equity financing.

Hours of Operation

We are available Monday - Friday

9 am CST - 4 pm

Central Standard Time

with a credit score of 690 or higher and steady monthly revenue. This ensures the borrower has a proven track record of managing finances responsibly.

with a credit score of 690 or higher and steady monthly revenue. This ensures the borrower has a proven track record of managing finances responsibly.

Merchant Cash Advances (MCAs): Revenue-Based Working Capital

Merchant Cash Advances (MCAs): Revenue-Based Working Capital